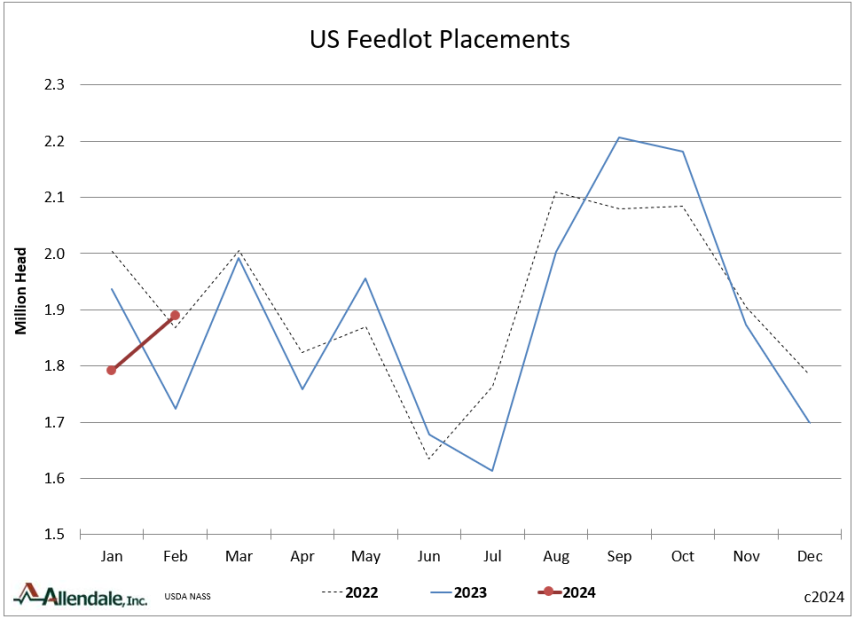

COF shows record February inflows. However...

Cattle on Feed was called moderately negative. The focus for this month's report was on the size of the increase for February placements. USDA reported +9.7% from the prior year to 1.890 million head. The bearish argument is this was over the average trade estimate of +6.4% (ALDL +6.8%). It was also a record placement for any prior February. This is a scary sounding number when everyone has become accustomed to low supplies. Keep in mind this is simply a make-up kill. January's weather issues hit that month by -7.5%. When you combine those two months the inflow is only +0.6% from last year.

Marketing's of finished cattle in February were counted 3.4% over last year. The expectation was +3.8% (ALDL +3.3%). There were not higher actual slaughter numbers last month. The increase is due to days on the calendar 2024 vs. 2023. Cattle on Feed as of March 1 comes to 1.3% over last year. The trade estimate was +0.9% from last year (ALDL +1.3%).