Best soybean close in nine sessions.

Grains

Allendale released the first of two outlook conferences set for 2024 this morning. The 2024 AgLeaders Conference Series consists of both a January and a July conference. This includes weather, supply, demand, price projections and even marketing/trading recommendations for grains and livestock. Registered subscribers can access Drew Lerner's weather comments until February 1 and our work indefinitely. https://www.allendalehub.com/winter-conference

We would not suggest Brazil's weather situation is fixed. It is not. The Center/West region will see a mixed profile over the next seven days, some area above normal moisture and some areas below. The second week forecast is now clearly below normal. The South will see below normal rains over the next two weeks. Weather right now, during the reproductive stage for the extreme majority of their crop, is the prime determinant.

Argentina is set for normal/below normal for one week then back to normal for week two.

Corn

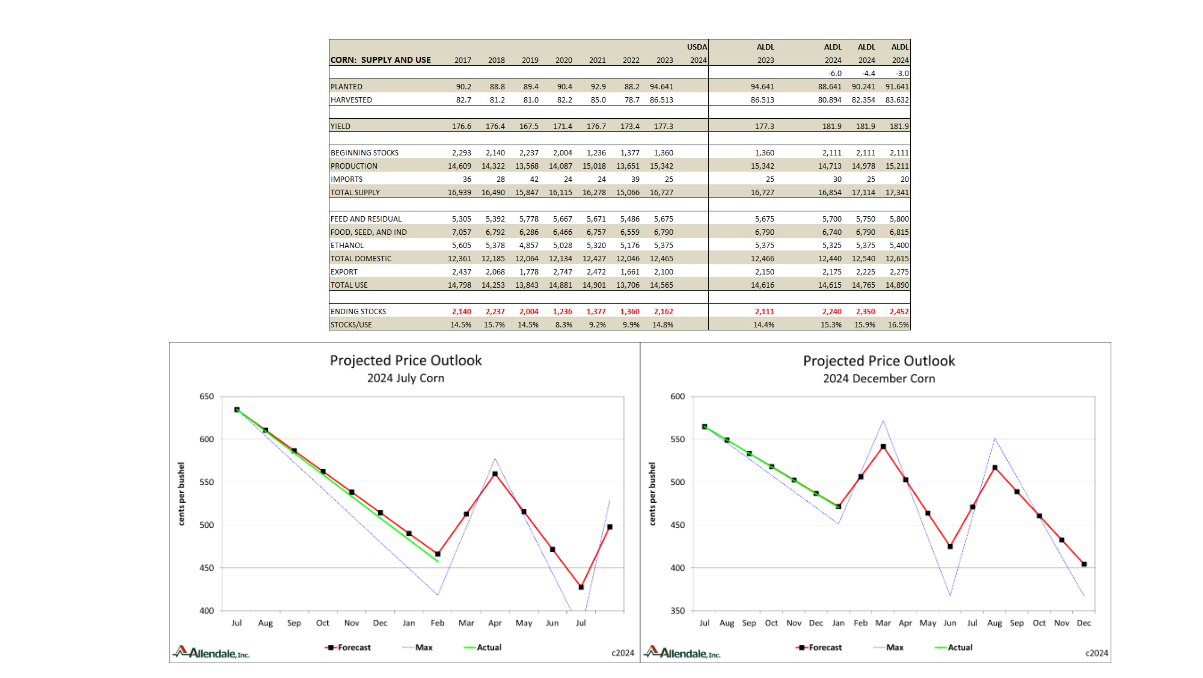

Corn traded mixed in a generally quiet session. Allendale released the 2024/25 outlook today.

Allendale released our first conference of the year this morning as part the AgLeaders Conference Series. The starting point for the new crop corn outlook obviously starts with the old crop picture. Heavy carry-in supplies from old crop as of August 31, 2.111 billion bushels (USDA 2.162), are a sharp jump from the prior year's 1.360 starting point. The main story for corn is very clear. Do we have reason to bring these stocks down and avoid even lower prices in the year ahead? New crop budgets are not looking positive. University of Illinois currently sees cash corn breakeven costs for new crop at $5.11. Their current budget suggests a loss of $154 per corn planted acre this year. That would be the worst loss of our 15 year database of Central Illinois crop farming history. They estimate the current old crop marketing year will see a loss of $144 per acre. Two serious hits are lined up. With that in mind our model scenario sees planted acreage -4.4 million from last year at 90.241. There are others calling for less of a drop but we don't see those as realistic at all. With a general average of 91.26% harvested we see that category -4.2 million from last year at 82.354.

Yields are of course a hotly debated issue. USDA's starting view of trend yield in 2023 was 181.5 bpa with a final actual number -4% at 177.3. That makes it five years in a row of below-trend yields. We do understand many people would want to suggest that means we'll also miss it this year. We missed it those years because there were moderate weather hindrances in those five years. Also remember, the prior 2014 - 2018 year period saw five straight instances of above trend yield. And further supporting the yield discussion remember that much of the ag community was discussion 2023 was a repeat of the 2012 drought. If you know exactly what weather will be in July, the first three weeks of August and the exact planting date this year you'll get the yield story right. We have no problem in starting the 2024 trend yield, what you get with average temperatures and average precipitation, at 181 bpa. Our 14.978 billion bushel production estimate would be the fourth best. When including beginning stocks and imports our 17.114 billion total supply estimate would be a new all-time record. It would also be 387 million over the 2023/24 total supply. So that's where we are at. Even with a much smaller starting acreage than many we still have a supply problem.

We see a 239 million bushel jump in total demand for 2024/25 to 14.765 billion. That pushes the implied ending stock at 2.350 billion. That would be the largest since 1987/88. As a clear reminder, it is stocks divided by usage that drives price, not just plain stocks. We show a stock number in our price modeling to you for simplicity. The 15.9% stocks/use would be over the 2023/24 level of 14.8% and the largest since 2005/06. As a disclaimer, the 2017/18 marketing year which ended at 14.5%, saw USDA monthly reports at/above those levels from July 2017 - February 2018. December 2017 corn futures, and the correct old crop ones after, traded $3.49 - $3.98 ¾ on those eight USDA reports. As we have stated very clearly for several years any ending stock number over 1.8 billion is trouble.

Though Allendale does look for clearly lower prices later in the year we are suggesting current prices are about where they need to be for now. A spring planting rally would push July to $5.60 and December to $5.42. Final expiration prices would be $4.28 for July and $4.05 for December. These are based off of our popular pricing model using similar years. In plain speak I, as the person who has made Allendale's price projections for over 20 years, would call these optimistic. We understand the extreme majority of our client base is in a tough situation. Whether they simply did not do any hedging this past summer, or blew out of hedges, a significant majority of US producers did not have protection on during this multi-month fall. On the old crop side everyone is holding full bins with no projection and watching prices fall almost daily. Our outlooks do give chances for higher prices later this year. But on these rallies it should be treated as selling opportunities rather than a time to get bullish.

We don't use USDA's projections as gospel. We do monitor their numbers though. They are with us for concern this year. On November 7 their annual Baseline Projections report used 2.111 billion for old crop stocks, -3.9 million for acres, total supply of 17.176 billion, stocks of 2.616 billion and stocks/use at 18.0%. Their next personal projection will be the annual AgForum Conference in DC on February 15 - 16. Their AgForum numbers do not typically deviate from the Baseline too much.

Two other groups released acreage estimates today. S&P Global suggested 93 million for corn and a Farm Futures magazine survey suggested 92.8. We don't see the implied -1.6 and -1.8 as realistic. If they are then are bearish price outlook would be even more bearish.

A newer Brazilian research group, Cogo Consulting, lowered their prior 12/8 view of Brazilian corn at 119.3 million tonnes down to 118.5 today. They are using Conab's starting acreage views rather than USDA.

El Nino and Argentine Corn Yields: Argentina plants corn mid-September through November. Reproduction, the phase where weather really matters, is in January an February. Over the past 25 years there were 8 with an ENSO reading of +0.5 during their yield determination (January). All 8 years posted above trend yields (+3.4% to +15.0%). The influence is relatively consistent.

March Corn Chart: The long term downtrend remains. A new low was made on Thursday. There is an upside intraday gap at the 12/29 close of 471 ¼ but that is not in the short term discussion. The downtrend remains in place until resistance at 466 is broken.

2022/23 Producer Marketing: Completed 2022/23 marketing year net of $7.01 (USDA seas. ave for Central IL $6.60). Previous hedges on 50% using options, 25% on 2/28/22 and 25% on 6/7/22, were lifted 7/26/22 for +56 4/5 cents (adj. to 100% of the crop nets +28 2/5 cents). Cash sales of 25% 1/18/23, 50% 1/26/23 and 25% 2/10/23 for net $6.73 via Cental IL.

2023/24 Producer Marketing: Profit of 163 7/8 cents from two prior hedges on 75% of the crop (123 cents when brought to 100% of the crop). Currently holding the third hedge on 75% enacted 11/13/23 using purchased CH 460 puts at 10 1/4/sold 520 CH calls 6 ¼ for net 4 cents. No 2023/24 cash sold. 1st hedge on 75% using short CZ23 futures were lifted on 5/1/23 for +68 4/7 (sales of 50% at 600 on 1/19/23 + 25% at 595 on 2/10/23 lifted 5/1/23 at 529 ¾). 2nd hedge on 75% using options were lifted 11/13/23 for +95 2/7 (sales of 50% on 6/16/23 using purchased CZ 560 put 35/sold CZ 640 call 27 for ((net 8 cents)) lifted 11/13/23 at 97 and 1/8 ((net 96 7/8)) + 25% 6/20/23 using purchased CZ 580 put at 41/sold 660 CZ 660 call 32 for ((net 9 cents) lifted 11/13/23 at 117 ¼ and 1/8 (net 117 1/8).

Corn Summary: We are in no way bullish corn. Our similar year based price outlook did suggest we should be nearing a winter low and starting on a temporary move higher into planting. For producers we continue to hold hedges. That may change in the coming days...Rich Nelson

Working Trade:

(11/30) Sold March 480 call 15, risk 19, objective 0. Closed 7/8.

Soybeans

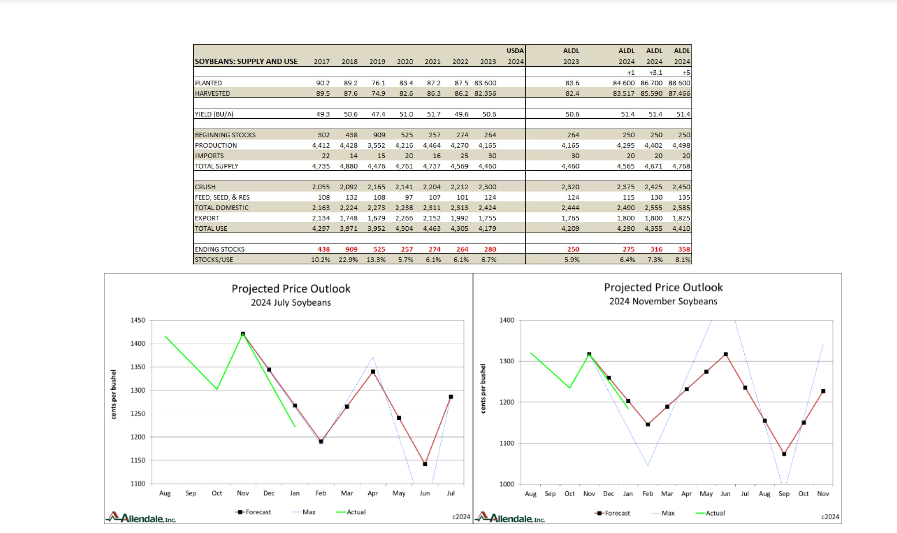

A much better than expected rebound was noted today in soybeans. It appears the market is finally looking at the extended Brazilian forecast. 1200 psychological support may have held on the dominant March.

Allendale sees the 2024 soybean story as a little different than corn. Our carry-in stocks of 250 million bushels, USDA is at 280, is not burdensome. They are larger than we expected to see at this point but not overly burdensome. The new crop discussion does show light concern with a potential $52 per acre loss on the U of IL budgets. That assumes breakeven cash soybeans at $12.22 per bushel. Their loss from the current crop is seen at $13 per acre. Our model scenario sees planted acreage +3.1 million from last year at 86.700. There are others calling for less of an increase but we don't see those as realistic at all. With a general average of 98.72% harvested we see that category +3.2 million from last year at 85.590.

On the yield end we are now looking at 50.6 bpa for the 2023 harvest. That was -4% from USDA's starting view of 52.0 trend. We do have to point out that soybean yields ended over USDA's view of trend in 7 of the past 10 years. Additionally, compared with many expectations this past June a -4% hit from trend is nothing. Our starting trend yield is 51.4 for the 2024 crop. Our 4.402 billion bushel production estimate would be the fourth best. When including beginning stocks and imports our 4.671 billion total supply estimate would be the fifth largest. It would also be 212 million over the 2023/24 total supply.

We see a 146 million bushel jump in total demand for 2024/25 to 4.355 billion. That pushes the implied ending stock to 316 million. That would be the largest in four years. Stocks/use, the determinant of price, would be 7.3%. That is also the largest in four years. On the price end our forecast suggests July futures would find value at $11.91 and November at $11.46 in the coming weeks then rally to $13.40 an $13.17 for spring highs. That would then be the high and a push to lows on the July to $11.42 and November at $10.74. These may seem like large price swings but keep in mind that implied $2.37 per bushel trading range for November this year is not at all out of bounds for soybean swings. On a personal note I am wondering if current price action itself is finding an early winter low.

We don't use USDA's projections as gospel. We do monitor their numbers though. On November 7 their annual Baseline Projections report used 253 million for old crop stocks, +3.4 million for acres, total supply of 4.710 billion, stocks of 244 million and a stocks/use of 6.5%. Their next personal projection will be the annual AgForum Conference in DC on February 15 - 16. Their AgForum numbers do not typically deviate from the Baseline too much.

Two other groups released acreage estimates today. S&P Global suggested 85.5 million for corn and a Farm Futures magazine survey suggested 85. We don't see the implied +1.9 and +1.4 as realistic. This potential profitability disparity between corn and soybeans is a bit more than this.

Here in January the range of reasonable Brazilian soybean crop estimates is from 149.2 - 158.5. USDA and Conab are at 157.0 and 155.3 respectively. At this time the trade is not seeing production declines at a level enough to support prices.

El Nino and Argentine Soybean Yields: In normal years soybean planting is limited to November and December. Yield determination, weather during reproduction, is from January - March. Over the past 25 years there were 7 with an ENSO reading of +0.5 during their yield determination (February). 6 years posted above trend yields (+3.2% to +22.3%). 1 saw below trend yields (-1.3%). The influence is relatively consistent. El Nino brings above trend yields to Argentine soybeans. At this time we are not yet seeing a change from normal precipitation to above-normal.

With USDA's recent revision of the 2023 soybean crop they now have ending stocks up to 280 million bushels. This number still has a lot of potential sway involved, different than corn. We compute a 200 ending stock as implying $14.00, 250 stock at $12.95 and 300 at $12.20. In our view, soybeans are at economic value. We will note there is still considerable movement still ahead on this balance sheet.

March Soybean Chart: The trend is down and we have a long ways to go to test chart resistance. However, today's good rebound in price could be the first sign of chart based life here. It is true new lows for the downtrend were made on Thursday. One positive is the 1200 psychological support has held. Lows of 1175 ¼ from 6/8 and 1145 ¼ from 5/31 are now the only support levels ahead. Resistance for this downtrend, drawn from highs of 11/21 and 12/28, is 1275 1/2. Bulls can also point to a good sized gap left to the upside, 1290 ¾ - 1296 ¾. Past that there is another gap at the 11/22 close, 1374 ¼. Are we now ready to discuss that upside chart gap?

2022/23 Producer Marketing: Completed 2022/23 marketing year net of $15.08 (USDA seas ave for Central IL $14.20). Previous hedges were on 40% using options (20% on 2/14/22 and 20% on 2/28/22 lifted 7/26 for +7 1/9 cents). Adj. to 100% of the crop nets +3 5/9 cents. Cash sales of 25% on 1/3/22, 25% on 1/17/22, 25% on 2/15 and 25% on 2/23 for net $15.05 via Central IL.

2023/24 Producer Marketing: Profit of 29 cents from two prior hedges on 75% of the crop (22 5/8 cents when brought to 100% of the crop). Curently unhedged and holding cash. 1st hedges on 75% using options lifted for net +60 7/8 cents. (50% sold on 1/19/23 using 1360 Nov puts 78 7/8/sold 1180 puts 17/sold 1500 calls 40 1/8 for net 21 3/4 cents + 25% sold on 2/15/23 using 1360 Nov puts 68/sold 1180 puts 12/sold 1500 calls 35 1/2 for net 20 1/2 cents. All lifted 5/2/23 at 86 1/8 (115/17 1/2/11 3/8 for 50% and 81 ¾ (115/22 1/4/11 3/8) on 25%. 2nd hedges on 75% using options expired 10/27/23 for net -31 7/8 cents. (Sold 6/30/23 on 75% using bought 1240 November puts 47 3/8 and sold 1460 calls 15 ½ for net 31 7/8, expired at 0 on 10/27).

Soybean Summary: The drier Brazilian forecast ahead is supportive. But we're really wondering if this downtrend may be subsiding simply because of psychology. We still suggest this market is undervalued from a balance sheet perspective. The market has disagreed with our view for three weeks but may now be more accepting of it. For producers we are holding cash beans unhedged...Rich Nelson

Trade Recommendation:

(1/17) Stand aside.

Wheat

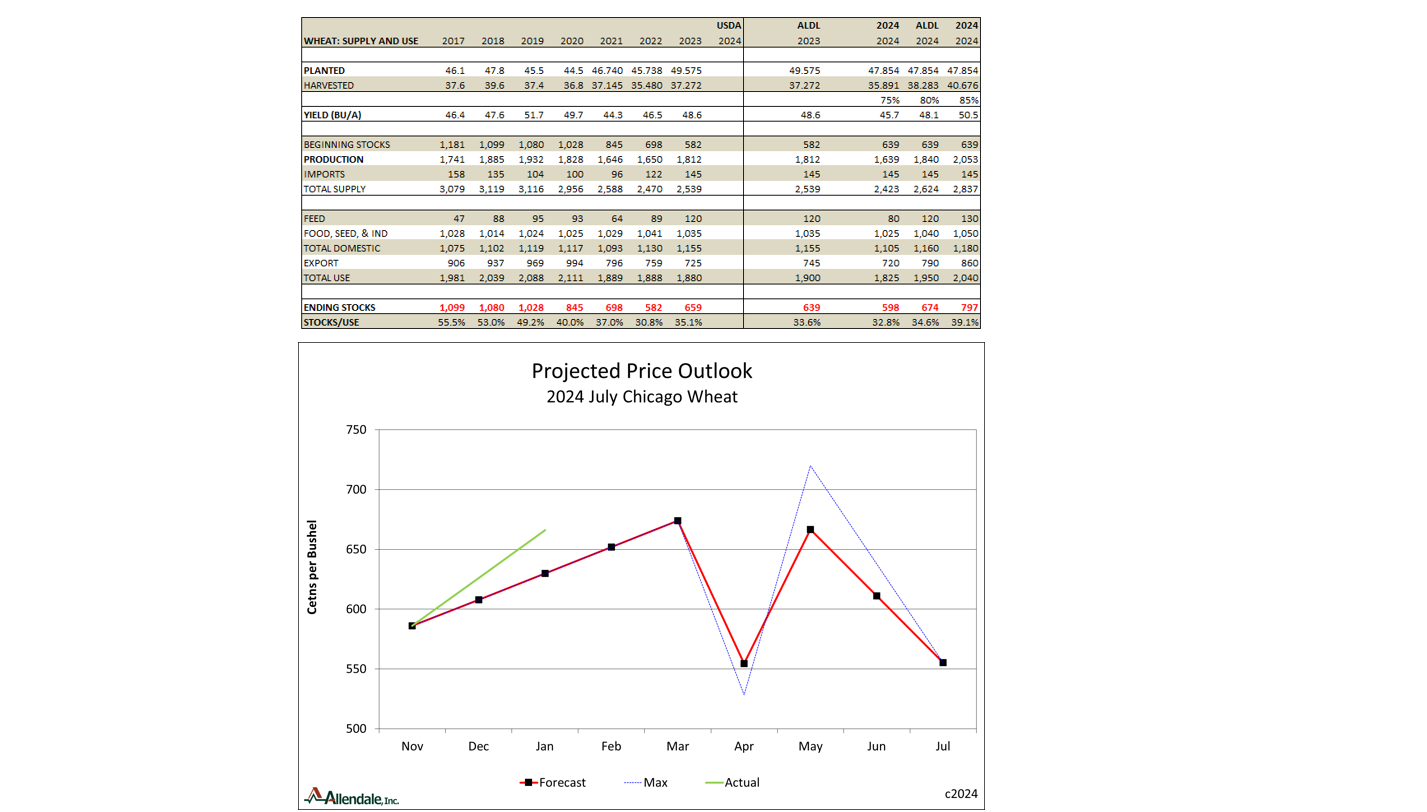

Wheat ended the day with mixed trade. Shipping disruptions are being discussed but this is not a reason to rally. The US Plains will soon switch from below normal temperatures to above normal. Additionally, good moisture is seen ahead.

For wheat we are nearing the end of the May 31 old crop marketing year. A start to the winter wheat acreage argument has already been made. Though USDA will adjust their January 12 survey of +2.2 million acres ahead in March, then June and lastly in September the general story won't change. Our old crop stock view is 639 million bushels (USDA 659). We see total acreage -1.7 with other spring +0.4 and durum +0.1. A 1.840 billion production would be the largest in four years. A 2.624 billion total supply would be the largest in three years. This would be +85 million from 2023/24.

We see a 50 million bushel jump in total demand for 2024/25 to 1.950 billion. That pushes the implied ending stock to 674 million and stocks/use to 34.6%. On the price end our forecast suggests July Chicago futures with a spring high to $6.74 and an eventual low of $5.54.

We don't use USDA's projections as gospel. We do monitor their numbers though. On November 7 their annual Baseline Projections report used 670 million for old crop stocks, -1.6 million for acres, total supply of 1.940 billion, stocks of 782 million and a stocks/use of 40.1%.

Two other groups released acreage estimates today. S&P Global suggested 47.225 million for all wheat and a Farm Futures magazine survey suggested 47.854. USDA 2023 is at 49.575. These two estimates are -2.4 and -1.7. Of interest the magazine survey of 825 farmers suggested an unusually large -2.1 decline for other spring. That's an oddly large hit for a small 11.2 million acre crop.

The wheat market continues to note cargo diversions away from the Red Sea. If there was a risk of no grain being transported then wheat prices would rally. Instead, with clear confidence the market will get the grain, the market is taking the extra transportation cost off the flat export bid.

SovEcon revised its view of Russian wheat exports in January down from 3.8 million tonnes to now 3.6. This is a little bigger deal than it sounds. This now makes it three months in a row where exports fell below last year. Nov was -0.9 mt from last year, Dec was -0.3 and Jan here was -0.2.

Wheat Summary: Russia's wheat exports in January are not expected to fall below last year levels. That marks three months in a row. Our price outlook suggests a little higher pricing but not a runaway bull market...Rich Nelson

Trade Recommendation:

(1/12) Stand aside.